An Overview of Bankruptcy

With the unemployment and foreclosure rates soaring, and our economy in a recession, many Americans are taking advantage of our federal bankruptcy courts as a solution for overwhelming debt. Bankruptcy is a viable legal option that gives a debtor in trouble the ability to reorganize or begin a new life by completely eliminating debt. Bankruptcy is a federal (country-wide) system of civil laws, rules, and procedures enacted to afford legal residents of the United States a solution to deal with unmanageable debts, when, for whatever reason, individuals or businesses are unable to pay as they come due. Besides the federal Bankruptcy Code, consumer protection laws, and state insolvency or exemption laws as they apply to individuals and business, all affect the options available for overwhelming debt. Most bankruptcies are for people, and called consumer bankruptcies.

Bankruptcy can accomplish a large number of goals, depending on what chapter is filed, and what is possible in each specific situation. Depending on your circumstances, bankruptcy can possibly help you: save your home by stopping foreclosure immediately, rebuild your credit by discharging or restructuring your debt, keep your home, car, and personal property, lower your car payments, stop wage garnishment, end harassing creditor calls, and stop all collection efforts, including lawsuits and license suspension.

Bankruptcy is in effect a lawsuit that is filed in federal court against creditors. The court administers the estate, or assets, of a debtor (a person or business who owes money to others) for the gain of his creditors (persons or businesses that are owed money). Usually people or businesses file for bankruptcy voluntarily, but sometimes they may be forced by a creditor into an involuntary bankruptcy proceeding.

Bankruptcies basically operate in one of two basic ways. Either all of the dischargeable debt is eliminated with no payments made through the case (Chapter 7 of the Bankruptcy Code), or else repayment plans are put into place for different categories of debts (Chapters 9, 11, 12, and 13). An attorney looks at a number of factors, such as income, expenses, assets, types of debts, prior filings, and long-term goals, to decide the proper solution. We at Spalding Law Center can help you accurately assess whether a payment plan is best for you, and which chapter best suits your needs.

The vast majority of individuals filing for personal bankruptcy choose to file under Chapter 7 or Chapter 13 (for individuals, couples, or people with businesses in their name). Corporations and other business entities usually file under Chapter 7 or Chapter 11. The following is a brief description of the four types of bankruptcy. The Chapter number refers to the section of the bankruptcy law, called Title 11 of the U.S. Bankruptcy Code.

Chapter 7 Bankruptcy is sometimes called a “liquidation,” or debt-elimination. It is the most common type of bankruptcy filed, and is what most people think of when they think about bankruptcy. Most people in Chapter 7 keep most of their property and wipe out, or discharge, most of their debt within a short period of time. Debt that is not eliminated includes student loans, domestic support obligations, divorce debt, government fines, and most tax debt. There are many exceptions and factors regarding qualifying, so it is best to talk to a lawyer to see if this is a viable option for you.

Chapter 13 Bankruptcy is sometimes called a “wage-earner reorganization” bankruptcy. It is a repayment of debt over a three to five year time period. All bills are consolidated into one monthly payment. Most people only have to pay back what they can afford to pay, rather than all of the debt. Calculating the repayment amount is complicated, best suited for a trained attorney, and is based on monthly disposable income, un-exempt equity in assets, and income as calculated by the “means test.” People who are advised to file a Chapter 13 include: those behind in their mortgage or car notes that they can afford to keep, those who could lose property in a Chapter 7, wage earners who have the ability to repay some, but not all of their debts, recent Chapter 7 filers, or those with unbearable tax obligations.

Chapter 11 Bankruptcy is a corporate reorganization bankruptcy for companies trying to stay in business. Some individuals with extremely large amounts of debt who do not qualify for Chapter 13 must file Chapter 11. It is a very complex and expensive type of bankruptcy, so most individuals try to avoid this chapter. Business entities have the option of filing for liquidation under Chapter 7, but those that seek protection while they continue to carry on routine operations while reorganizing their business debt, file under Chapter 11. Corporations, partnerships and sole proprietorships are all the types of businesses that file, as personal assets of the business shareholders are not involved. But both the personal and business assets of a sole proprietor are at risk since a sole proprietorship does not have a separate legal identity from its owner.

Chapter 12 Bankruptcy is solely for family farmers. This chapter is very uncommon in urban areas since it helps a small class of rural people.

The “New” Bankruptcy Law

You may have heard that there are new bankruptcy laws making it difficult to file bankruptcy now. Well the new law is not that new anymore. The Bankruptcy Abuse Prevention and Consumer Protection Act of 2005, or BAPCPA, was enacted in 2005. It is not necessarily true that it is “harder” to file bankruptcy now. Even though the new bankruptcy law stipulated new requirements for filing, Chapter 7 and Chapter 13 is still an option for most people. Now debtors are required to complete a court approved credit counseling class before filing a case (these are specific classes required by the federal government intended for bankruptcy qualification, and NOT your run of the mill credit counseling firm services), a debtor education course after filing, and complete a means test to determine eligibility to file for Chapter 7, or a minimum that must be paid to unsecured creditors in a Chapter 13 case. There are definitely more hurdles to filing now, but for the most part it just means that attorneys need to do more work in each case, and there is a greater premium now on the knowledge and experience of the attorney. We at Spalding Law Center have that experience and knowledge to obtain the best possible relief for you under the new law. We have staff that practiced bankruptcy long before the law changed, and during the law change, when many practitioners abandoned the practice of bankruptcy after it became much more complicated for firms to handle. If you are wondering if you can file for bankruptcy under the new law, call our office today. You will be glad you did.

Chapter 7 - Chicago Bankruptcy Attorneys

Chapter 7 Bankruptcy Overview – What is it?

Chapter 7 Bankruptcy Overview – What is it?

Chapter 7 Bankruptcy is sometimes called a “liquidation,” “straight bankruptcy,” or debt-elimination. It is the most common type of bankruptcy filed, and is what most people think of when they think about bankruptcy. The basic purpose is to provide people with unmanageable debt a clean slate by eliminating all qualifying debts. These qualifying debts are considered “dischargeable,” and examples of these types of dischargeable debts are: medical bills, credit cards, most judgments from law suits, deficiencies on repossessed vehicles and foreclosed homes, unsecured personal and payday loans, and most other basic consumer debt. Most people in Chapter 7 keep most of their property (such as a home and car) and wipe out, or discharge, most of their debt within a short period of time. Debt that is not eliminated includes student loans, domestic support obligations, divorce and property settlement obligations, penalties based on fraudulent behavior, government fines, and most tax debt.

The vast majority of debtors filing a Chapter 7 do not pay anything towards their dischargeable unsecured debts, and their debts are completely and permanently eliminated. Credit reports later reflect that those debts were “discharged through bankruptcy.” Debtors keep all their property and eliminate all of their dischargeable debts in about 99% of Chapter 7 cases.

That being said, the liquidation bankruptcy contemplates an orderly, court-supervised process in which the trustee takes a look at the financial picture of the debtor, collects the unprotected assets of the debtor’s estate, liquidates or sells them, and uses the cash proceeds to pay the debtor’s creditors. A creditor holding an unsecured claim will get a distribution from the bankruptcy estate only in this situation, and if he also files a proof of claim with the bankruptcy court. All of this is subject to the debtor’s right to retain certain exempt property, as laid out by state law exemptions, and the rights of any secured creditors to the assets. State law exemptions allow everyone to keep property up to a certain dollar figure. So assets worth less than that dollar figure are exempt and therefore protected from seizure, and cash proceeds from a liquidation that are above that dollar figure are not exempt. For example, in Illinois, if you are a couple filing bankruptcy, then $30,000 of equity in your home, $4,800 of equity in two cars, and $8,000 worth of other property are all protected. Exemptions in most states, including Illinois, are generous enough to protect the property of the average person. Exemptions can get complicated though, so it is best to call a knowledgeable attorney to help you handle a Chapter 7 in order to protect as much of your property as possible. Spalding Law Center can advise you about your assets and strategize your case so that you reach the most successful outcome possible. Sometimes clients come to us after they have already made a poor decision in managing their assets, and our options become more limited. It is always better to speak to us before you make any major financial move.

Since most cases have little or no nonexempt property, an actual liquidation of the debtor’s assets usually does not occur! We call these cases “no-asset cases.” After this determination is made, the debtor goes on to receive his discharge releasing him from personal liability for the dischargeable debts. Debtors generally receive the discharge about 4 months after the petition is filed.

Chapter 7 - Who can file?

In addition to individuals and couples, partnerships, sole proprietorships, and corporations are eligible to file under Chapter 7. There are certain restrictions for individuals to file when they are repeat filers. If you have filed a case before, it is best to speak to us about the nature of your old case to determine your current eligibility.

Chapter 7 business liquidations work very similar to Chapter 7 individual consumer bankruptcies. Much of the company’s assets are sold and the net proceeds are divided among the creditors of the business. The business then ceases to exist after liquidation and distribution. Larger partnerships and corporations often intend to continue to do business, and therefore usually prefer to file under Chapter 11. If you run a failing small business in which you have not built up a lot of name recognition or accumulated lots of business assets, Chapter 7 may be right for you. Give us a call to discuss your options!

Chapter 7 Bankruptcy Process - What Happens?

The entire bankruptcy process, from start (at filing) to finish (at case closing upon discharge), usually lasts about 4 months. The first step is to gather financial documents and a completion of credit counseling certificate. We advise our clients not to obtain the certificate before meeting with us, because: there are potential timing issues that can cause complications for the case, only select agencies are government approved, and we can help facilitate the process so that it is easier on everyone. We then utilize the financial documents, other information that you may give, and your credit report, to prepare your bankruptcy petition.

Automatic Stay

After we file your petition and initiate the process with the court, you are protected by the automatic stay, which instantly goes into effect. The automatic stay is injunctive relief that prohibits most creditor collection activities. This includes filing or continuing on with a lawsuit, billing for payments, collection calls, suspending a license in some circumstances, and reporting the debt to the credit reporting agencies as unpaid (rather than discharged).

A Meeting of the Creditors, otherwise known as a Trustee Meeting or 341, is held about 4-6 weeks after filing. In almost every case there is just one meeting. The meeting is informal and takes place in an ordinary conference room. Creditors rarely show up to this meeting. The trustee, who is not a judge, but a person appointed by the court to oversee the case, reviews the petition with you and us, confirming the information that we included in the petition. He asks routine questions about particular items on the petition, with a particular emphasis on your assets and income. Most meetings last under 10 minutes. It is natural for many debtors filing to be afraid or anxious before the meeting. As our client, there is no reason for you to be afraid, as long as you have been honest and forthright with us. We have the experience to know what red flags will set off a trustee, and to advise you ahead of time if we see potential problems. The trustee is on the hunt for people who are hiding assets or trying to defraud the system. He has no desire to harass or scare the common person. We prepare our bankruptcy petitions in such a thorough and precise fashion, that the trustees usually have virtually no additional questions to ask our clients beyond the routine core interchange. Most of our clients tell us after the meeting, “That’s it? That was easy.” After the meeting, usually the only thing left for you to do is to keep your address current with the court, and to wait for the discharge to come in the mail about 2-3 months later. Some people choose to selectively pay back certain debts, such as those to family members, but that is of course not legally required. We at Spalding Law Center provide guidance and support every step of the way. If you are considering a Chapter 7 bankruptcy, please give us a call today.

Chapter 13 - Illinois Bankruptcy Lawyers

Chapter 13 Bankruptcy Overview – What is it?

Chapter 13 Bankruptcy Overview – What is it?

Chapter 13 Bankruptcy is sometimes called a “wage-earner reorganization” bankruptcy. Chapter 13 of the United States Bankruptcy Code provides individual consumers a way to consolidate their debts into a three to five year payment plan, under the protection of the federal court. The code refers to the individual consumer filing as a “debtor;” one who owes a debt. Most debtors only have to pay back what they can afford to pay, rather than all of the debt. If the consumer has sufficient steady income allowing him to pay all current living expenses and also have a portion leftover each month to devote to a payment plan, then filing a Chapter 13 is an excellent solution when that leftover portion is not enough to pay off ALL debts, or to comply with creditor demands. Unsecured debt is generally discharged, while secured debt is restructured. Calculating the repayment amount is complicated, and best suited for a trained Chapter 13 attorney, and is based on monthly disposable income, un-exempt equity in assets, and income as calculated by the “means test”. Debtors enjoy the ease of an affordable payment plan, the end of collection calls, and a stop to spiraling interest, which we can quickly become out of control if not stopped. People who are advised to file a Chapter 13 include: those behind in their mortgage or car notes that they can afford to keep, those who could lose property in a Chapter 7, wage earners who have the ability to repay some, but not all of their debts, recent Chapter 7 filers, those suffering from an inability to cope with the collection efforts by creditors of non-dischargeable debts, and those with unbearable tax obligations. If any of these scenarios sound familiar to you and you are wondering if you should file for Chapter 13, please give us a call and we’d be happy to discuss it with you.

Chapter 13 - Who can file?

Individual and couple debtors with regular income may file under Chapter 13. They must be United States residents and have unsecured debts of less than $360,475 and less than $1,081,400 in secured debts (as of April 2010; these “amount adjusts” every three years). Corporations and partnerships are not eligible to file under Chapter 13, but self-employed individuals and individuals who own unincorporated businesses can file Chapter 13. Also, a debtor from a prior bankruptcy case that was dismissed “with prejudice” within the prior 180 days cannot file within the prohibited time frame. Please give us a call today to see if you are eligible to file for Chapter 13.

Chapter 13 Bankruptcy Process - What Happens?

We submit a Chapter 13 “plan” to repay all or part or of your debts in monthly installments over a three to five year time period. The calculation of your plan payments is complicated since it involves many variables, but generally, the plan is not usually based on what you owe, but rather, is based on your ability to repay creditors, along with other factors, such as the types of debt you have. You can make certain decisions about whether to keep certain secured debt, for instance, but must pay certain tax debts and child support arrears in full. Typically for most unsecured dischargeable debt, such as credit card and medical debt, you only pay as much as you can afford, even if that means the plan only pays pennies on the dollar. Since the calculation is based on your income and expenses, generally speaking, what you have left at the end of the month goes into the plan, as detailed in the monthly budget we draw up for you and file with the court. We have your plan approved by the court, and then it becomes effective. Creditors are prohibited from collecting their claims directly from you after the bankruptcy filings as long as your case is active with the court and you are current with your payments.

Your first plan payment is due a month from the original filing date. You send your monthly plan payments to a “Chapter 13 Trustee.” The trustee in turn distributes the funds to the creditors pro rata, as called for in the plan. You are discharged from further liability for the remainder of your dischargeable debts upon completion of the plan payments.

Just like a Chapter 7, the court will schedule a Meeting of the Creditors about 4-6 weeks after filing. Creditors rarely attend the meeting. The trustee will review the petition filings and plan that we submit on your behalf, with both of us. The trustee will ask you to confirm the information and ask questions about your financial situation to make sure the proper budget for you is laid out. The trustee will inquire about any concerns he has about the feasibility of the plan at this time.

At the conclusion of the plan period, and assuming no complications, your case will come to an end, and you will be granted your discharge in bankruptcy. You must attend a debtor education course with a certified agency before the discharge can be issued. The Chicago Chapter 13 Trustees offer this class for free at their offices, or we can arrange for you to take the class at your home, any time you would like, with an agency that charges a small fee. Either way, the course is about an hour and a half of your time.

Chapter 13 bankruptcy filings are difficult. You will need the best representation to protect your rights, and to make sure your repayment plan pays your creditors at the best rate possible. Spalding Law Center has the experience to guide you through all the proceedings. Please give us a call for a free consultation today.

Real Estate Short Sale - Chicago Short Sale Attorneys

Can you no longer afford to keep your mortgage payments current?

Can you no longer afford to keep your mortgage payments current?

Have you found that due to the real estate market crash, your house is no longer worth what you paid for it, and that your home value continues to decline so that any hope of building equity in your home feels like a pipe dream?

Perhaps you have tried selling your home, only to learn that the market will not bear a listing price that is more than what you owe on your home.

If so, you are not alone. In the first quarter of 2011 more than 28 percent of U.S. homeowners with mortgages owed more than their properties were worth, as values fell the most since 2008, per Zillow Inc.

There is a solution! A short sale may be your best option to control your mortgage debt and stay out of bankruptcy and foreclosure proceedings.

A short sale is a real estate transaction in which the proceeds from the sale of a property are less than the amount owed on the mortgage, and the mortgage lender accepts the amount offered when releasing its lien and foregoing foreclosure. The seller turns over the proceeds of the sale to the lender, and the debt may be fully satisfied. The homeowner must negotiate with the bank’s loss mitigation or workout department prior to the sale to accept the amount offered, to see if the lender is willing to release its lien on the home for less than the outstanding balance including interest and penalties.

Although a short sale is typically executed to prevent foreclosure, the decision by the bank to proceed with discounting a loan balance is predicated on its self-interest in recovering as much of the amount owed on the property as possible, in the most economical way. Not all lenders will accept a short sale if it makes better financial sense for them to foreclose and suffer a smaller loss. When making their decision, banks look at extenuating circumstances, such as the current real estate market and the borrower’s financial hardship. Indeed, the bank faces carrying costs with foreclosure as well as expenses with receiving and maintaining foreclosed properties.

Spalding Law Center can give you the straight facts to determine if a short sale is in your best interest. We represent homeowners and investors who need to sell properties they cannot afford to keep. We think this can be a great option, as mortgage lenders do generally want to keep your property out of their foreclosed inventory. It is a great benefit for you to be able to sell your property without owing the lender any money or having a foreclosure on your credit report.

It is important that you seek legal guidance when negotiating the short sale with the bank to ensure that your obligation is indeed fully satisfied. We have seen a number of bankruptcy clients come to us after they still owed money to the bank subsequent to a short sale. Without representation you could be required to sign a promissory note to cover the difference between the purchase price and the total amount still owed on the mortgage. We will make sure this does not happen. We will explain the process for a successful short sale during a free initial consultation with you. We will take you through every step of the process to list the property, handle all documentation and negotiations with the bank, reach a deal with a buyer, and close the transaction to finalize the deal. The lender pays all but a minimal amount of your legal fees and the costs of the transaction out of the money your buyer brings to the transaction. Our legal staff is experienced and has in-depth knowledge of the local real estate and mortgage lending community. Combined with our bankruptcy experience, we have the experience you need to best advise you to the most cost-effective solution to your mortgage problem. Give us a call!

Creditor Harassment - Chicago FDCPA Creditor Harassment Attorneys

Creditor Harassment

Creditor Harassment

Do you have creditors badgering your friends or family about your whereabouts? Is your employer warning you that your job security is on the line due to creditors calling you at work? Are you afraid to answer the phone because of the abuse you receive from bill collectors? If you are a victim of this type of behavior, Spalding Law Center can help you put an end to your creditor harassment.

Debt collectors know that it can be embarrassing to owe money. There are plenty of good collectors out there that do not take advantage of this fact, and treat debtors with respect while operating above board. There are a few bad apples though, that give the debt collection industry a poor image. These collectors lack respect and will pursue whatever means they can to embarrass debtors into paying. They take advantage of the fact that it can be even more embarrassing to be accused of not paying one’s debt. They often decide that it makes better business sense for them to practice abusive behavior if it will lead to their desired result of payment, and to suffer any penalties as a cost of doing business. Debt collectors position themselves so that they wield the power. It is important that consumer debtors understand their rights under federal law, so that instead of being victims, they can play a part in stopping the culprits.

Fair Debt Collections Practices Act (FDCPA)

Congress understands that creditor harassment is a problem, and so it enacted the Fair Debt Collections Practices Act (FDCPA) to halt the behavior and make it illegal for debt collectors to ignore its regulations when attempting to collect debts. Since the bad creditors unfortunately continue to break the law, hoping that you will cave under their pressure since you are not aware of your legal rights, your best weapon is knowledge.

Spalding Law Center would like to educate you so that you will know if any of your creditors are breaking the law. If you have a debt collector that is performing some of these prohibited actions, then Spalding Law Center will stop the harassment. Not only that, we will help you recover any actual damages without you having to pay any attorney fees. If you need to also file bankruptcy, an average settlement will be enough to cover the expenses of your bankruptcy case.

The FDCPA is the federal law that governs the way third party debt collectors who regularly collect debts operate. Many states have their own laws similar to the FDCPA. The FDCPA, or the “Act,” covers personal, family, and household debts, but not business debts. For example, collections by collection agencies collecting on credit card, medical, and vehicular debt are covered, rather than actions by Chase bank, a hospital, or Ford Motor Credit, collecting on their own accounts.

A collector is allowed to contact you in person, or by mail, phone, or fax. He may not contact you at an inconvenient time or place without your permission. This means he cannot call before 8a.m. or after 9 p.m. to your job after you tell him this is not acceptable. You can stop the action by writing a letter to the creditor demanding that he do so. Upon receipt, the creditor may acknowledge that he will stop or take specific action, but must cease the prohibited contact. This does not mean you no longer owe the debt. You must still pay for it or file bankruptcy if you are unable to pay. If you hire an attorney, your debt collector must contact your attorney instead. Our bankruptcy clients already take advantage of this service that we offer, even when their creditor action does not rise to the level of harassment. Without an attorney, a debt collector of yours may contact other people, but generally only once to find out your home and work location and phone number. He also may not reveal to the third parties that you owe him money.

After you are first contacted, your collector must send you a written notice explaining to whom you owe money, what amount you owe, and how you can dispute a mistake. If you reply with written notice that you do not owe the money within 30 days, the collector must cease contact. He is not allowed to collect during those 30 days. If he sends you a bill or other proof of the debt, he can renew legal collection activities.

Prohibited Debt Collection Practices

Creditors that do not adhere to the process mentioned above are in violation of the Act. There are a number of other actionable offenses.

Debt collectors may not threaten a lawsuit when there is no actual intent to sue at the time the threat is made. Courts have ruled that when a lawsuit is not practically feasible due to a low balance, under $250, for example, then you can assume there is no intent to sue. Also, if you have an out of state collection agency, you can generally assume that they do not have anyone licensed to practice law in your state. It would therefore be impossible for them to file suit when making the threat. The employees at the collection agency cannot imply that they control the decision to litigate. For example, an employee at a collection firm cannot say that he will refer the matter to an attorney and that he WILL sue. A non-lawyer cannot make this decision.

Debt collectors cannot threaten to take action that cannot legally be taken. For example, they cannot threaten to have you arrested.

As mentioned, the collectors cannot disclose the debt to third parties other than a spouse or attorney. Voicemails count as a prohibited communication when the message discloses the debt owed.

Debt collectors may not use any false or misleading statements. There are several offenses dealing with false statements. They cannot falsely imply that they are attorneys or government representatives. The debt collectors also cannot imply that they operate or work for a credit bureau. They cannot falsely represent the amount of the debt or whether or not papers being sent are legal forms. They cannot falsely imply that you have committed a crime. They cannot use a false name. They also may not give false information about you to anyone, including a credit bureau.

As mentioned, collectors cannot communicate with debtors after having reason to believe that the debtors are represented by legal counsel. Verbal notice is acceptable, but the contact information of the attorney must be provided.

As mentioned, collectors cannot communicate with a debtor at an inconvenient time or place, such as his place of employment after being told the calls are not permitted. The collectors cannot communicate with a debtor before 8 a.m. or after 9 p.m.

Debt collectors may not harass, oppress, or abuse debtors or any third parties they contact. For example, they may not call you names, use threats of violence or harm, or use obscene language or curse. They may not call multiple times a day to annoy someone. They may not publish a list of consumers who refuse to pay the debt (except to a credit bureau).

Debt collectors may not engage in unfair practices when they try to collect a debt. For example, they may not collect more than the amount of the debt, deposit a post-dated check prematurely, contact via a postcard, or threaten to take your property unless this can be done legally.

Debt collectors must disclose during every phone call, “I am a debt collector attempting to collect a debt and information obtained will be used for that purpose.” They must also disclose in subsequent communications, “This is from a debt collector.”

Your Right to Sue

You have the right to file suit against a collection agency that performs one of these prohibited actions within one year from the date the law was violated. If the collection agency is a law firm, you can still sue. If you win, you may recover money for actual damages you suffered plus an additional amount up to $1,000. You can also recover court costs and attorney fees. A typical settlement is $1000-$2000. If you are able to record the violation on tape, your recovery could be ten times that much. The type of violation, damage suffered, and available proof can make a big difference here. It is very important that you do not delete any debt collection voicemails. You should also keep any collection letters and any contemporaneous notes that you are able to make regarding the time, place, and details of the call.

Bankruptcy Laws Also Stop Harassment

Besides writing a demand letter to debt collectors to cease contact, or resorting to a lawsuit under the FDCPA, you can also rely on bankruptcy laws to put an end to creditor harassment. Your creditors will receive notice of the filing immediately after you have filed either a Chapter 7 or Chapter 13 bankruptcy. The automatic stay instantly goes into effect to protect you. Unlike the FDCPA protection in which just third party debt collectors must cease contact with you, ALL creditors are prohibited from continuing collection actions against you after the automatic stay goes into effect through bankruptcy. Most creditors understand this prohibition quite well, and are good about heeding the power of the bankruptcy protections. In that rare instance in which a creditor continues to willfully defy the automatic stay, we will gladly motion the Bankruptcy Court to impose severe sanctions on the violating creditor. If you have a creditor harassing you that will not seem to go away, then give Spalding Law Center a call, and we will gladly step in!

Credit Repair - Chicago Credit Repair Services

Your New Life After Bankruptcy

Your New Life After Bankruptcy

When you have your discharge papers and your bankruptcy is behind you, take a big sigh of relief! You have just accomplished a large milestone in your life. Pat yourself on the back for taking control of your life and putting your credit on the road to recovery. So many people ignore their debts and turn a blind eye to a plummeting credit score due to a large debt load, and possibly late payments. You have taken charge of your life and given yourself the gift of a new beginning. While you are experiencing a financial rebirth, don’t forget why you filed bankruptcy to begin with. Do your best to improve your financial life so that you do not fall into the same situation again. Spend less time approaching life from a consumer standpoint valuing material goods. Refocus your life by spending more time focusing on your mind, body, friends, family, and spiritual life. Clearing your life of clutter, both mentally and physically, is a helpful reminder that we do not need all the “stuff” our culture sometimes makes us feel that we do. It robs us of our lives. Start truly living yours! You have earned your new life, so enjoy it!

After you have had a chance to relish in your new life and the freedom it affords you, it is time to start thinking about rebuilding your credit after bankruptcy.

Rebuild Your Credit

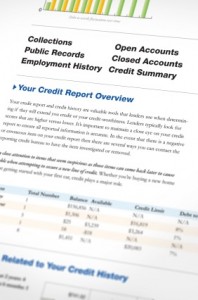

Your credit matters. Most people know that your credit score affects home and auto loans, but did you know that it could affect home and auto insurance rates too? Employers may look at your credit report as well. Don’t throw in the towel and give up on your credit just because your credit has been poor due to years of debt, and because you filed bankruptcy to solve your debt problem! Instead, make good on the major progress you have made by greatly improving your income to debt ratio, and keep on at it! Rebuilding credit after bankruptcy is not all that difficult and you may be able to progress faster than you may think. A poor credit score will not haunt you forever. It is a snapshot into your current credit risk at a particular time, and the score changes gradually as you change your relationship with credit. Start by figuring out where you are, by pulling your credit report.

Accurate Credit Reporting

You should check your credit report about two to four months after you receive your bankruptcy discharge. Keep the discharge that you receive from the court in a safe spot. We recommend that you keep it as long as possible, or at least 10 years. We can send you a copy as well when we close out your file with us. Order your credit report from one of the three credit bureaus (Equifax – 800.525.6285; Experience – 888.397.3742; or TransUnion – 800.916.8800) so that you know exactly what’s on your credit report, and you can begin to understand it better. You can contact each bureau directly, or you can connect thru www.AnnualCreditReport.com. You are entitled to a free report from each bureau once every 12 months, as a result of the Fair and Accurate Credit Transactions Act; the FACT Act.

When you request your own credit report, it is scheduled as a “soft inquiry” and doesn’t count against your score. Check for mistakes. Make sure debts that were discharged through bankruptcy list as just that, rather than as due and owing. The last thing you want to happen is go to the trouble of filing for bankruptcy and then find out many years later that discharged debt still shows as a current obligation. Creditors and credit reporting agencies also make mistakes if someone enters a wrong social security number or account number. A paid account could be listed as a charge-off too. Follow the instructions listed on the credit report for reporting errors. A few months later obtain a copy of your report from the second bureau. Report any mistakes. Then two months later obtain your third report. Spreading out your three free credit reports over the year is the best way to check up on your report to make sure mistakes are being cleared up, since creditors are likely to correct mistakes with all three bureaus when they follow up on one reported mistake. This is why we urge our clients to order a paid three-source report from all three agencies when we file the case; so that the free annual reports are best optimized in the year following the bankruptcy discharge.

It is better for you to be educated about your credit rating, even if it is not as high as you wish. If you never inspect your credit report, you will never know what possible mistakes are bringing down your score. You have the right to have anything that is incorrect investigated and possibly removed. Federal laws require that the credit bureaus verify all disputes. The law says that if they are unable to verify your dispute, it must be removed from your file. Your discharged bankruptcy, items older than 2 years, charge-offs, repossessions, late payments, and inquiries are easier to remove than newer open accounts. Frankly, the creditor is just not too concerned with the account anymore when this is the status. Creditors may not want to take the time to verify a dispute if already paid, or may not even be able to find the account information to verify a dispute, if they have already written the account off the books due to bankruptcy. It is more difficult to dispute the open accounts that are still active, such as for your recent bankruptcy, current past due and collection accounts, judgments, and tax liens. These creditors have your account open as due and owing, and so are expecting to receive payment, and therefore much more likely to verify credit information for you.

Life after Bankruptcy

When you have your discharge papers and your bankruptcy is behind you, take a big sigh of relief! You have just accomplished a large milestone in your life. Pat yourself on the back for taking control of your life and putting your credit on the road to recovery. So many people ignore their debts and turn a blind eye to a plummeting credit score due to a large debt load, and possibly late payments. You have taken charge of your life and given yourself the gift of a new beginning. While you are experiencing a financial rebirth, don’t forget why you filed bankruptcy to begin with. Do your best to improve your financial life so that you do not fall into the same situation again. Spend less time approaching life from a consumer standpoint valuing material goods. Refocus your life by spending more time focusing on your mind, body, friends, family, and spiritual life. Clearing your life of clutter, both mentally and physically, is a helpful reminder that we do not need all the “stuff” our culture sometimes makes us feel that we do. It robs us of our lives. Start truly living yours! You have earned your new life, so enjoy it!

After you have had a chance to relish in your new life and the freedom it affords you, it is time to start thinking about rebuilding your credit after bankruptcy.

Applying for Credit

This is an especially important time to not go around haphazardly applying for loans or credit of any kind. Applying for several credit cards within a short period of time means multiple requests for your credit information, or “inquiries,” will appear on your report. Inquiries into your credit report except those made by you will lower your credit score further.

Do not take on any obligations that you cannot repay based on the terms you agreed to. Do not, under any circumstances, co-sign for a credit card or any type of loan, for anyone. This WILL come back to haunt you, and you should just consider yourself responsible for the entire loan, if you do not heed this advice. Also, even if you are applying for a loan at one place, many inquiries could be generated if your credit application is sent to many different lenders. There is good news though, for the home and auto loan process. If you have multiple inquiries within a short amount of time due to the loan application process for these items, most credit scores are not affected. The inquiries are lumped together and treated as a single inquiry.

Speaking of which, if you are able to get a car loan, and can afford it, then finance a car loan. We can give you the information for a few car finance companies that specialize in helping bankruptcy filers. Think this through though. A car note will help you rebuild your credit if you have a manageable monthly payment and keep the account current. You must get as much positive information on your credit report as you can, after all. Make certain that the lender you choose reports to the bureaus. A “buy here; pay here” lot will often NOT report, and should therefore be avoided. Your interest rate will probably be high if you apply for a loan immediately after your discharge, but your timely payments will reflect positively on your credit report. Try to make extra payments and pay your car note off early if you can. Only then should you trade your car in for an upgrade and repeat the process. At that point, you will be making great progress in reestablishing yourself.

It is a horrible idea, however, to put yourself right back where you started with an expensive car, accompanying expenses, and a high monthly payment and interest rate. We see too many people that are working for their car. Although making regular timely payments on a car note is good for your credit, it is not good if your car expenses divert precious funds from other necessary expenses as well as your emergency fund, so that you have negative monthly income. If you can get by for a while with public transportation, you may be amazed at how much disposable income you are able to free up. If public transportation is not available, consider paying cash for a used car that is fuel-efficient.

A better option for the near future may be to take out a new credit card. Misuse and other factors, some beyond your control, were the problem that got you into trouble; not the card itself. You can probably qualify for one, even if it is a high interest rate. Most likely you will need to start with a secured credit card that is secured with your savings account, but that is ok. You need to start somewhere with positive information on your credit report. Do not carry your card with you all the time, or to the mall, since this is not a green light to go on a shopping spree. Just use it for necessities, such as for groceries, utilities, or gasoline if you have a car. Pay off the balance at the end of each billing cycle! If you absolutely must carry a balance on any credit account, make sure that you are only using 25% of your available credit. These necessities should already be in your budget, so it should not be a problem to pay off the balance on the secured card. If you have adjusted your mentality as previously mentioned, you can do this. If you can’t control the spending on even a secured card with a low credit limit, then do not obtain a credit card yet.

This information should help you repair your credit, whether or not you have filed bankruptcy. It most likely took you many years to harm your credit score, so do not expect to fix it overnight. If you did file bankruptcy to eliminate a large amount of outstanding debt, then you have already made major progress on the road to recovery. These steps will put you further down that road. It is possible to have a nearly perfect credit score just one or two years after a bankruptcy discharge. With a little effort and time, you can do it!

Pay Your Bills on Time

Make sure you pay your bills on time. No excuses. Even paying one day late can have an impact on your score and interest rate. When you mail payments, make sure it is in the mail 7 days before the due date. If you have any debt that was not discharged in bankruptcy, focus on paying that off. Did you spend several months in a payment plan working on your bankruptcy fees? Now that you are used to setting aside a little money, keep it up until your non-discharged debt, such as your parking tickets or student loans, are paid off. Municipalities report parking ticket and traffic violation debt to all three credit bureaus. After 6-9 months of nonpayment the debt can turn over to a collection agency that can then tack on additional fees and interest. After you have paid your non-discharged debt off, keep putting those funds aside. Now you should put those funds in a savings account set aside for emergencies. If you are only able to put aside $50 a month, it will build a good foundation and add up to a significant amount of money quickly.

If you find that you are still encountering roadblocks to improving your credit score after following these instructions, then give Spalding Law Center a call to inquire about using our unique credit education and assistance program. There are no gimmicks to the customizable program. For a small flat fee you can have one on one education on improving your credit score, budget coaching, have someone handle for you all the correspondence and follow-up in correcting credit report information, and have meaningful regular contact to encourage credit improvement. We at Spalding Law Center are committed to making sure you have the best financial life possible. If you are having problems obtaining credit and find yourself stuck with a low credit score that will not budge, give us a call and we will discuss how our credit repair service can help!